March 20, 2012

Our Glorious Ocean of Hydrocarbons

A FRIEND OF MINE recently posted on Facebook this story from Investor's Business Daily detailing the United States' oil reserves, which may in fact be much larger than originally thought. Far from only having 22 billion barrels of proven reserves, IBD's John Merline reports the United States has as much as 400 billion barrels of oil recoverable using present technology, and theoretically much more beyond that.

Now, I don't know about you, but when I hear that, it makes me think that we're sitting on top of a glorious ocean of hydrocarbons, just waiting to be exploited and put to good use. We already know, of course, that we have vast amounts of natural gas available to us -- so much gas, in fact, that the price has fallen to roughly $2 per million BTU and our producers are routinely "flaring" the stuff -- that is, burning the excess that can't be transported or otherwise used. So if we've already let the horse out of the barn when it comes to natural gas, why not do the same with oil production?

I mean, if you consider the tradeoffs inherent to this equation, you've got the environment and global warming concerns (1) on the one hand, and an amazing -- incredible -- unbelievable sum of money on the other (2). So to me, it's worth considering whether what could be done with all that money outweighs any environment problems that may result. You know, perform a cost-benefit analysis.

Now, if we use that 400 billion barrel figure mentioned above, that's roughly $42.8 trillion worth of oil at today's prices. Leaving aside the economic impact of all that oil for a moment, we could do a lot with $42.8 trillion.

Of course, part of the reason to pursue this idea is that oil prices will fall as a result. This is important, considering oil acts as a lubricant for the engine of our economy. Lower oil prices mean lower input costs. Lower input costs mean lower prices and greater profits. Lower prices and greater profits means more prosperity. It especially means more prosperity for regular working people, whom all our politicians and talking heads have forgotten about over the past decade or so. But you may rest assured they are still out there, slogging away.

You see, there are plenty of people out there for whom the New Economy isn't really working out. They may not have the skills or the education to knowledgeably design a bridge or program a computer -- and for some, going back to school to gain that education isn't a realistic prospect -- but they sure know how to do a lot in terms of the strong-back, heavy-labor tough stuff associated with oil production. In oil-rich North Dakota, where unemployment is at 3% and a truck driver for an oil producer can make upwards of $100,000 per year, regular working people are making out like bandits and presumably having a great time doing so. There's no reason why we shouldn't make these opportunities available to as many people as we can.

Additionally, it stands to reason that of those trillions of dollars, a heck of a lot of it will go to the Government in tax revenues -- from the workers themselves, who will be making money hand over fist, and from the companies producing the oil, which will be making money hand over fist. Imagine what could be done with that money. It's entirely possible we might be able to afford all the programs we currently have without having to borrow money to pay for them. For that matter, we might even be able to afford new programs that could provide great benefits to the people making use of them.

Imagine if the oil we produced let college students pursue their studies without having to shoulder immense student loan debts. Imagine if it provided health care for millions of people who couldn't otherwise afford it. Imagine if it meant we could lower tax rates for everyone. The possibilities are endless -- and it's not as if we have any good reason to wait.

The only possible reason that makes sense for not exploiting the oil, of course, is that it leaves us the last man standing when everyone else runs out. But even that's taking long-term thinking to an irrational extreme, because a) as Keynes famously said, in the long run, we are all dead; and b) as economics students know, we will never actually run out of oil, because people will quit using the stuff once better alternatives become available. (It's the old college-economics analogy about being stuck in a room stocked full of pistachio nuts; I forget who came up with it. Anyway, the idea is you're never going to crack all of the pistachios, because eventually you'll give up searching for the nuts amongst the growing, and eventually giant, number of discarded shells).

Of course, if there are better alternatives available, we should keep researching them -- they might come in handy someday, and it will keep our scientists at work. (Even oil may prove inferior to an engine powered by a thorium laser). But at the same time, we shouldn't go searching through the couch cushions for loose change when we've got a crisp $100 bill sitting on the kitchen table, either.

One final point to mention regarding the environmental aspects of oil production, which seems to be a major driver in terms of opposition to looking for more oil. Aside from the fact oil production today is necessarily much cleaner than it was 40 or 50 years ago (and do you think BP wanted to pay $20 billion to clean up its spill in the Gulf?), it's worth noting where the oil itself would be produced. Our major deposits are located in Montana, Wyoming, and western North Dakota, and it is there that much of the expected surplus would be wrung out of the ground.

Folks, I don't know about you, but I don't have any plans to visit Wyoming, Montana, or western North Dakota anytime soon. (Nor do I plan to visit Alaska's North Slope). It's one thing to be upset if an oil refinery will be built next to your house; it's another thing entirely to be upset because someone's building an oil refinery 1,500 miles away, in a state where you don't live, have no plans to visit and wouldn't even think about except for the fact some activist acquaintance posted about it on social media. If people in these locales are willing to drill for oil, we should not only let them, we should encourage them -- because we'll reap the benefits for their sacrifice.

--------------

1. I have to say that all this concern over global warming doesn't make sense to me. The last time we had a warm period, the Vikings had self-sustaining colonies in Greenland. Greenland, for God's sake. To be more precise, though, there's nothing to indicate the costs of global warming would outweigh its benefits -- and that's the key issue for me (and other people who are blasted as "climate change deniers"). The benefits include longer growing seasons, lower food prices, less hunger and less world instability. Also, shipping and resource exploitation will become easier, particularly near the poles. With those things as the result, we should welcome global warming with open arms, not waste trillions of dollars in a futile attempt to stop it.

Unfortunately, however, I don't think we'll be so lucky. I subscribe to The Twilight Zone theory of global warming, which is based on an old episode of the show ("The Midnight Sun"). This theory stipulates that everyone calling for drastic action to stop global warming will find, in something of a twist ending, that we're actually in for a severe bout of global cooling. I base that on solar cycle theory regarding global temperature patterns (i.e., it's the Sun wot does it), known past history regarding said patterns (e.g., the Maunder Minimum), and associated research, particularly out of Russia -- the last place that wants any global cooling to happen.

As one might expect, the costs associated with global cooling would be significant -- and would lead to shorter growing seasons, higher food prices, more hunger and perhaps famine in less-developed parts of the world, and greater world instability.

2. It's worth noting the $42.8 trillion figure is a low estimate for the value of the oil, as there may be as many as three trillion barrels of oil to exploit. Based on some back-of-the-envelope calculations, that would provide us with enough money to ensure every household in America had a solid gold toilet.

Yeah, So I've Been Busy These Last Two Years

I HAVEN'T POSTED since December 2010? God. It's amazing what a new profession and graduate school training does to a guy. Anyway, I'm hoping to devote time again to the blog in the near future, because there's so much I would like to write about, but I haven't had the time or the energy to pursue it. But let's see if I can't change that!

December 07, 2010

Thanks for Saving Us, You Rotten Bastards

THE OLD SAYING has it that no good deed goes unpunished. The chairman of the Federal Reserve, Ben Bernanke, and everyone else who works for the place ought be forgiven if that phrase has ruefully gone through their minds as of late.

After all, all the Fed did was save us from a second Great Depression. For accomplishing this feat, a success that can only be described as unparalleled in the history of monetary policy, this august institution has found itself under attack from all sides. It would be one thing if these attacks came only from the usual suspects, who have their own reasons for lambasting the Fed at every turn, but increasingly the Fed has become an easy target for attacks from people who ought know better.

The usual suspects, of course, are the old hard-money types who have a ridiculous attachment to gold – to my ear, they even say the word as if they just discovered some in the back of Sutter’s Mill -- and the idea of a gold standard. They view our current monetary arrangements as a disaster, resulting in deficits and rampant inflation, and long for the supposed security of the metal.

Your correspondent finds this a bit daft, as real estate – or any real property – does the same job without the unpleasant tax treatment and costs of storage, but that’s a story for another day. I have no doubt these folks are morally upstanding people who only want the best for their families and society as a whole, but I do think they’re wrong on this one, and have been for a long time.

But it’s not the goldbugs or their criticism of the Fed that irks me – like the poor, they shall always be with us. What does annoy me is the criticism that comes from people who really should know better – or who are blaming the Fed for failures that should be laid at their doorstep.

Exhibit A, in this instance, is U.S. Sen. Bernard Sanders, I-Vt. Sen Sanders, reportedly an actual socialist, does not like the fact that over the course of the past few years, the Federal Reserve loaned out some $3.3 trillion to various corporations and financial institutions throughout the world. Inconveniently for the Senator, this did not result in any actual loss to the Fed – in fact, it made a profit on the loans – but it still, according to Sen Sanders, resulted in a secret “backdoor bailout” on a “jaw-dropping” scale.

One wonders what alternative Sen Sanders would have wanted. After all, the Fed made these loans when the credit markets had completely seized up, and no private institution wanted to loan money to anyone. Had no money been available, it would have caused a cascading failure of private enterprise, and would have made today’s 9.8 percent unemployment rate look like a walk in the park.

Sen Sanders seems more piqued that the Fed did not, in his words, force “banks receiving assistance to step up lending to small businesses and to ease credit for consumers.”

Well, whose fault is that, one wonders? Perhaps Sen Sanders ought look at the Department of the Treasury, to say nothing of the lawmakers whose policy approaches can only be described as schizophrenic. Look how they handled TARP:

GOVERNMENT: Great news, everybody! We’ve got a $700 billion fund from Congress to help out banks and industry!

BANKER: Oh thank God.

SECOND BANKER: Praise the Lord!

THIRD BANKER: That’s great, but we don’t need it. Thanks, though.

GOVERNMENT: But you have to take the money too.

THIRD BANKER: What?

GOVERNMENT: Look, people are panicking. If they see Phil and Ted here took the money while you didn’t, there’s going to be a shitstorm and it won’t do anyone any good. So everyone has to borrow money even if they don’t need it.

THIRD BANKER: Well, if it stabilizes the system …

GOVERNMENT: Great. Just sign here.

(THIRD BANKER signs).

GOVERNMENT: OK, great. Wait a minute! How much are you paying your people? AND YOU’RE DOING THAT WITH OUR MONEY?!

THIRD BANKER: What? You wanted us to take the money, and –

GOVERNMENT: THIS IS COMPLETELY OUTRAGEOUS! WE SHALL HOLD HEARINGS ON CAPITOL HILL AND LAMBASTE YOU IN FRONT OF THE AMERICAN PEOPLE! CONSIDER YOURSELF SERVED, YOU SCUM.

-------

Then, of course, there was the whole issue of capital reserves.

-------

BANKER: Thanks for the loan. Now we’re adequately capitalized again.

GOVERNMENT: Good. Glad we could help. Oh, that reminds us: WHY AREN’T YOU LOANING MORE MONEY TO SMALL BUSINESS AND CONSUMERS?!

BANKER: What? You wanted us to improve our capital ratios, so we did.

GOVERNMENT: THIS IS COMPLETELY UNACCEPTABLE!

BANKER: OK, so let me get this straight. You want us to improve our capital ratios but loan more money out to people, all at the same time.

GOVERNMENT: PRECISELY!

BANKER: Those goals are completely contradictory. So which one of those do you want us to do?

GOVERNMENT: BOTH.

SECOND BANKER: But we checked with accounting and they said the numbers don’t add up.

GOVERNMENT: HEARINGS! CAPITOL HILL!

---------

Of course, the most scorn can be dumped upon the Government’s infamous $787 billion stimulus program. That a stimulus program was necessary is not in dispute; it absolutely was, and anyone who says otherwise is playing political games. But its design was so amazingly flawed, and in many cases so incredibly stupid, that in the end it was far less effective than it could have been.

After all, that’s $787 billion. There are roughly 306 million Americans, so that works out to roughly $2,572 for every man, woman and child in America. Let’s further say $287 billion would be spent on necessary things like roads, bridges and other construction projects we’ve been meaning to get around to eventually. That leaves $500 billion dollars, or $1,634 for every man, woman and child. If that $500 billion had been directly distributed to the American people, you’d have solved a hell of a lot of the problems right there. I mean, if a typical family got a check for $6,700 from the Government, and many of those dollars got spent, the multiplier effect would be incredible. Even if much of it was used to pay debt, it would free up a hell of a lot of cash flow.

Instead, the Government somehow managed to spend hundreds of thousands of dollars on each of the largely make-work jobs they created, along with protecting their most important constituents – those on Governmental payrolls – from the ravages of the economic storm. Those in the private sector, meanwhile, got a tax cut of … oh, eight bucks a week.

So I do hope you’ll pardon my skepticism when the same people, who thought eight dollars a week would spark an economic recovery Croesus himself would envy, cast scorn upon the one institution that actually has known what it's doing during this whole mess. I also hope you’ll pardon my amazement that people who couldn’t run a hot-dog stand if their lives depended on it now demonize an institution that, just a short while ago, saved the entire financial system from careening into an abyss.

December 04, 2010

Why Your Liberal Guilt Trip Doesn't Impress Corporate America

NOTED WITH AMUSEMENT: the squawks of fury and disbelief from commenters over at The New York Times -- and undoubtedly elsewhere -- over news that PayPal, along with Amazon, have severed their ties with WikiLeaks. WikiLeaks, of course, is the shadowy group slowly releasing a cache of myriad American diplomatic cables in an attempt to subject Foggy Bottom to the Chinese water torture.

I can't for the life of me figure out why people are upset with these companies. For one thing, WikiLeaks is arguably engaged in conduct that violates federal law, which isn't exactly conducive to convincing companies they ought do business with them. Besides, here's a newsflash, folks: this is what happens when you give the Government such extensive power that it only has to snap its fingers to get things like this done.

I mean, yeah, that's really a tough decision for the businesses in the middle. On one hand, they can cooperate with the Government and give it what it wants, thus making the situation go away. On the other, they can stand up to the Government, thus causing the FBI, the Department of Justice and anyone else who wants in to show up and cart off all their records, interrogate their executives and essentially bring their business to a screeching halt.

If you don't like that, then get to work on inventing a time machine. That way you can travel back to 1912 and warn the people they ought vote for Taft. More realistically, you can fire up iTunes, put on some Shoskatovich, and weep softly as the mordant strains of the strings play through your speakers. (I suggest his Chamber Symphony, Op. 110a, particularly part IV. Yes, there's a reason those first notes sound like harsh knocking on a door).

True, some people have suggested the way to show one's disapproval of these actions is to stop doing business with the companies in question. But let's be honest: 29.8 percent of the people now approving such suggestions would sooner cut off their pinky fingers than actually cut ties with the folks providing them valuable and useful services, while the remaining 70 percent don't actually do business with the firms in question, making their approval moot. (What about that last 0.2 percent? As they say in business, that's not material).

But let's play pretend for a moment and say that enough people did stop doing business with these firms to make it noticeable on a balance sheet. You know what would happen then, right? No, the companies wouldn't change their decisions. They'd lay off a bunch of low-level employees who had nothing to do with the matter at hand, then shift the laid-off folks' work onto the remaining staff. Way to stick it to The Man there, angry customers blaming the companies for making sound business decisions.

As radical as it might be these days, the only practicable solution is to somehow convince our elected geniuses that the Government's bureaucracy ought not have the power to utterly crush companies for doing business with people it does not like -- or for that matter, doing anything else. Would that lead to some distasteful scenarios down the line? Yeah, probably. But there's something to be said for having a Government that must wait for a guilty verdict before it starts knocking in heads.

June 11, 2009

Report: Consultants to Blame for Venezuela-Coke Fiasco

By HARRIS SCHWED

Financial Rant

Venezuela Bans Coke Zero,

Citing Health Concerns

-------

Calls for Invasion Grow

------

A "Rare Win" for Embattled

Brand Managers

CARACAS -- The Venezuelan Government yesterday banned the sale and distribution of Coke Zero, citing health concerns about the popular zero-calorie drink, in a move expected to cause "considerable distress" to the drink's bottler, Coca-Cola FEMSA SA de CV, and the Venezuelan people.

Health Minister Jesus Mantilla announced the move through the government's news agency.

It's unclear what led the Venezuelan Government to ban Coke Zero. Oddly, however, some observers in the South American nation are casting blame towards Coke brand managers Irwin Cholmondeley and Edward "Ned" Callahan. Those in the capital say Messrs Cholmondeley and Callahan appeared on President Hugo Chavez's popular television show, "Alo Presidente!" and encouraged the Venezuelan leader to take swift action against Coke Zero.

"Yes, I remember it," said Caracas bricklayer Hernan Martinez, as he was headed to work yesterday morning. "It was during the 27th hour of Chavez's marathon session last week. These two guys came on and started going on about infraccion del gusto and capitalismo imprudente. Then, when I went into the corner shop this morning, these men from the distributor were taking the Coke Zero away."

"Also, they took away the beer," Martinez said. "Something about -- how do you say it? -- 'taking back the High Life.' "

ALO PRESIDENTE! A video still from state-owned Corp. Venezolana de Televisión shows Messrs Cholmondeley (left) and Callahan elaborating on the "fundamental, capitalist evil known as Coke Zero" during President Hugo Chavez's weekly television program. President Chavez was reportedly quite alarmed to hear about how Coke Zero had created poor health among those exposed to it. Symptoms, according to Messrs Chomondeley and Callahan, included "anxiety, disturbed sleep, minor instances of paranoia, and concern over how certain people would pay their mortgages."

A clip of the show also shows Mr Callahan complaining of sore ribs and neck pain, which reportedly resulted from being tackled by a Coke Zero-crazed Troy Polamalu.

Reaction to the Government's move has been swift and strong in some quarters. Edison Paez, a Maracaibo storekeeper, complained the Government was robbing him of considerable profit.

"What the hell?" Paez said. "First they nationalize the staple good producers, and now they're forbidding honest Venezuelans from drinking Coke Zero -- a beverage, I might add, that was one of the few profitable things I could sell after the Government imposed price controls. Now what am I supposed to sell? Frescolita? The stuff tastes like bubble gum, for God's sake."

"If this keeps up, my store's going to have less stock than a Russian department store in 1985," Paez said.

However, not everyone was opposed to the move. Irina Tucupita, a hospital nurse, said she understood why the Government acted as it did.

"Those poor men. I saw them on the broadcast, and clearly this Coke Zero drove them entirely insane," Tucupita said. "So I can see why the Government decided to ban it."

WARNINGS: The Government has posted signs like these in major cities to spread word of the ban.

In the United States, observers said they thought the Venezuelan Government's move would have "minimal impact" on Coke Zero as a brand, but agreed it was "a rare win" for Messrs Cholmondeley and Callahan.

"These guys have been getting their asses kicked from Anchorage to Kuala Lumpur," said soda industry analyst Mark Piotrowski, of High Water Mark Brokerage LLC in New York. "Although this victory is a small one for them, it is a victory nonetheless, and as such it must be appealing."

When asked if rival PepsiCo Inc. could gain market share from the dispute, Piotrowski said, "I don't understand."

But opposition to the move is growing in Washington. A mid-level State Department official warned that, although Venezuela "really wasn't on our radar screen," other elements could take swift action to deal with the situation.

"We've got enough problems on our plate without worrying about how Chavez is going to further destroy his country's economy," the official said. "But it's not us he has to worry about. For one thing, taking any carbonated beverage product away from regular citizens will cause considerable societal discontent. For another, he doesn't seem to realize who he's dealing with. I mean, he's going to have to answer to the Coca-Cola Company."

June 09, 2009

The Most Dangerous Game

TWENTY THREE PERCENT. That's how much the workers affiliated with the Boston Newspaper Guild will have their pay cut, now that they've rejected a proposal from The New York Times Co. to cut their wages, implement furloughs, cut their benefits and make other changes to their contract. If there's one word that sums up the reaction from my colleagues in the newspaper business, it is: "Wow" -- and for a variety of reasons!

But after looking into it, I can't say the result surprises me all that much.

For one thing, Guild members were essentially asked to pick their poison during the most recent round of negotiations. A 23 pc wage cut, although stunning on its face, may for many members be preferable to the entire package presented them, which involved an 8.3 pc cut in wages, five days of unpaid time off, and changes to health and pension benefits. Add everything together in that proposal, and it doesn't take much to see the cuts inherent in that would also be dire.

As it happens, you can run the numbers and see for yourself, thanks to the Boston Newspaper Guild's handy calculator. In my case, I used the Guild's top-scale for a reporter at the Globe, which is $1,387.15 a week, or roughly $72,133 per annum. Losing 23 pc of that works out to an annual cash loss of $16,590. But when you add in all the benefit changes the New York Times had proposed, the annual cash loss was still $15,639 for a worker with a family!

Among those changes was a proposed pension freeze -- and it's no wonder many members said no, given the math. A pension freeze is a killer, as anyone who benefits from such a plan knows. The reason, of course, has to do with the eventual payout. As the Guild's calculator showed, a freeze would over time cost each worker well into the six figures. Using my example above, a worker with ten years in the plan would have his benefit frozen at about $1,100 a month. With a maximum payout of about $3,300 if the worker made it to 30 years, that works out to leaving $2,200 a month on the table. Over 20 years, that's roughly $529,000.

Yes, that's right. $529,000.

Also, for those wags wondering how much said worker could get if he got a 100 pc cut in his wages, think about how long it might take to get to that point. If the worker survives just one more year, he increases his monthly pension benefit by about $110 a month. Over 20 years, that's $26,400. So if you figure the ship's going to sink anyway, and you're going to sink along with it (or get thrown overboard prior to hitting the iceberg), voting to accept the Globe's plan makes even less sense. If I was in the Globe's unit, I'd take the pay cut and find a way to make it work.

So after looking at it, I can't say I would blame anyone in the Boston Guild for voting one way or the other on the contract proposal. I only hope the Boston local can convince its members of that -- because the margin of the vote was so close: 277-265. (Wow).

I mean, I've been involved in similar situations, in which everyone argues passionately about how to vote on a contract proposal. But in the arguments I've been involved in, the argument has usually been a way for everyone to let off steam. Then, when the vote comes in, it's usually something like 123-3 one way or the other. This vote was so close, and the stakes were so high, that it has the potential to make for a lot of angry members. I do hope, however, that's not the case in Boston.

So, to sum up for all of you wondering why the Guild voted the way it did, think of it this way. Basically, the Guild's members had a choice. They could get their crap sandwich on a sub roll or a trendy flatbread.

Of course, the real question remains unanswered -- just what will come down the pike.

Supposedly, the Globe lost $50 million last year and was on track to lose $85 million this year prior to the cuts, according to the Times. But I'd love a bit more elaboration from the company about this. Certainly, in looking through the Times' financial reports, there's no real breakout just for the Globe itself -- most of its results are reported on a consolidated basis among all of its newspaper operations. Go look for yourself if you don't believe me.

That said, there's no denying the Times' overall financial picture has worsened -- and to my mind, is actually pretty dire. Consider the following comparison of key statistics from the Times' '08 annual report:

Goodwill: $661.2m

Stockholders' equity: $504.0m

Now consider the reasonable reaction to this news:

BUTTHEAD: "He said goodwill." Uh huh huh huh huh huh!

BEAVIS: Yeah! Heh heh hrmmm heh heh! Goodwill sucks!

This basically explains, to my mind, why the New York Times won't close the Globe anytime soon. After all, how much of that goodwill -- an accounting term to describe the premium inherent in overpaying for an asset in order to acquire it -- is wrapped up in the Boston Globe, for which the Times paid $1.1 billion back in the day? I'm guessing it's still rather a lot, despite recent impairments. Plus, if the Times suddenly had to close the Globe, how much would the Times have to writedown or expense as a result -- not just in terms of goodwill, but in PP&E, severance costs, and so on? It's not like they can just close the place and have done with it.

Also, what's interesting in the Times' reports is that stockholder equity is a key metric for evaluating the various loans extended to it. That's not an issue now because of how those metrics are calculated -- for one of its big loans, the Times had about $568m in breathing room at the end of the first quarter. But again, if the Times suddenly decided the Globe had to go, just how much breathing room would the Times have after all was said and done?

Oh, and what happens if things get worse? In 2011, the Times will have one of its revolving credit lines -- which now has $287 million outstanding in borrowings and letters of credit -- expire. Unless everybody gets well really soon, I can't believe their lenders would keep the terms as generous as they are now. Already, the Times' debt is below investment-grade. Oh, and remember that big $250 million loan from Carlos Slim Helu? It's got an effective interest rate of 17 percent -- and a whole bunch of covenants that restrict the company's capacity to take on additional debt. (They also prove Mr Slim is a financial genius, but that's neither here nor there).

So if you ask me, what the Times really could use right now is cash.

There are three ways to get cash. First, you can borrow it, but the Times probably would like to avoid that. Second, you can earn more and stop spending as much of it, which the Times is naturally trying to do. Lastly, you can sell assets to raise it. If you ask me, Door Number Three is probably becoming more palatable all the time to the suits in New York. As with all companies, they know full well their lenders will have no compunction about slamming them to the wall if the lenders think it will serve their interests.

And the Times has plenty of things it can sell. Like a roughly one-sixth stake in the Boston Red Sox, for instance. It could sell some of its papers elsewhere in the country, of which it has 15 or so. It could even sell the Globe itself -- and I'd be stunned if the Times wasn't actively considering just how to do that. Besides, think of the savings on aspirin alone. Could be in the millions.

June 03, 2009

When Job Interviews Get ... Interesting

AS A JOBSEEKER, I was rather stunned at reading this great story in the Wall Street Journal about the lengths to which certain companies will go when it comes to interviewing prospective employees. The more novel tactics reportedly include:

-- requiring a prospective employee to provide 12 references

-- requiring applicants to bring their own lunch -- and three years' worth of W-2 statements

-- having prospective employees pitch other applicants as best for the job

-- performing a play with other applicants ... on the side of a highway.

-- asking inappropriate questions, such as how an applicant would react to the boss's gay son making a pass at them during an office Christmas party.

What, exactly, are these companies thinking? If you don't treat people with respect when you're in the process of hiring them, how do you expect them to treat your business? Let's say a company, XYZ Widget Corp., hired five people after subjecting them to a particularly cruel interview process, and interviewed a total of 50 applicants during that time frame. What would happen?

Well, at the very least, you can be sure the 45 people who didn't get the jobs would complain in most unflattering terms about XYZ Widget -- and to pretty much everyone with whom they came into contact. There's an old theory that says the number of people who know any given secret is the square of the number who have been told about it. So if that held in this case, you'd have 2,025 people who weren't all that fond of XYZ Widget Corp. Arguably, that could be broken down into the following subgroups:

* The 45 rejected applicants, who now hate the company and have secretly vowed revenge on its operation.

* The friends and family members who know the applicants well -- we'll call this number one-quarter of the remainder, or 495 people -- who now find the company appalling and make a point of studiously avoiding its products and services.

* The remaining three-quarters of the pool, totaling 1,485 people, who will remember the applicants' stories and make a point of discreetly avoiding doing business with XYZ Widget, much less apply for a job there.

Now, let's take the five people XYZ Widget actually did hire. It could be they end up loving their jobs, and become valued, productive employees. But it's a fair bet to say that XYZ Widget might not be the best place to work, based on its interview practices. Accordingly, two or three of the employees might jump ship once the economy improved. The fourth might end up performing at marginal capacity -- good enough to keep on, but not good enough to really sparkle or shine, which is ideally what you want from an employee. As for the fifth employee, well, he's probably a lawsuit waiting to happen.

Besides, what happens when the economy turns around? XYZ Widget's reputation -- which will stay with it -- will undoubtedly hinder its attempts to find qualified applicants when the available labor pool is small. That will accordingly mean lost opportunities in future for the company -- especially if applicants XYZ would have wanted for its team join the competition.

Now, this is not to say there aren't places for being tough during the interviewing process. Speaking personally, I don't mind a good challenge and would take a tough line of questioning as a chance to give as good as I got. But if faced with some of these questions, I would be inclined to ask some of my own. Like, "Are you well?"

The Untold Story of the U.S.-China Financial Summit

By HARRIS SCHWED

Financial Rant

BEIJING -- U.S. Treasury Secretary Timothy Geithner and Chinese Vice Premier Wang Qishan, and their respective subordinates engaged Tuesday in a financial summit between the world’s two economic superpowers, engaged in a “testy but ultimately useful discussion” during the talks, according to sources.

Despite the unusually frank nature of the back-and-forth, both sides agreed they had reached a consensus on the situation facing the two countries – namely, that the U.S. and China are completely and utterly stuck on their current course of action, whether they like it or not. A transcript of the exchange, which the Financial Rant obtained at great risk to its sources, makes this clear. The transcript follows:

---------------

SECRETARY GEITHNER: That was a fun question and answer session with the kids at Peking University, Mr Vice Premier. I can’t tell you how much I enjoyed being laughed at by a bunch of coddled Commie punks.

VICE PREMIER WANG: We are striving to achieve the openness you have in your own universities, Mr Secretary. We appreciate your patience with the students and trust they enjoyed the experience.

SEC GEITHNER: They certainly did enjoy it! That’s the problem. I’d be fine if a few of them enjoyed the experience of a re-education camp, that’s all I’m saying. I get enough of this crap back home.

VP WANG: You are right, of course, in that backbreaking agricultural labor often re-energizes the mind after strenuous months of studying. But we have many things to discuss.

ASSISTANT SECRETARY SMITH: Which reminds me -- you got any of those barbecued pork bun thingies? Those rule.

(General agreement among American delegation).

ASSISTANT VICE PREMIER YU: Yeah, we just ordered some.

ASST. SEC. SMITH: Sweet!

(A break for char siu bau ensues).

SEC GEITHNER: Now, where were we? Oh, right. Yeah. Now, look. You know our credit’s good, right? AAA rating from Standard and Poors? The world’s largest economy and all that? A GDP of $13 trillion?

VP WANG: Uh, you owe us $768 billion.

SEC GEITHNER: Right! So a few more billion here and there won’t really make much difference.

VP WANG: Well, no, but look, this is kind of getting out of hand. Besides, it’s not like we can just foreclose on California if you decide some day that you won’t pay us.

SEC GEITHNER: Which reminds me – how would you like Guam?

VP WANG: GUAM?!

SEC GEITHNER: Sure, why not? I mean, what are we doing with it? None of us here has ever been to Guam, and none of us ever will. You could use it as, I don’t know, a base for shipping lanes or something. It’d be a steal at $75 billion.

VP WANG: For that kind of money, we could buy Hawaii!

SEC GEITHNER: Oh. Well, yeah, but think of the prestige value of buying Guam. It’d be kind of like when we bought the Gadsden Purchase from Mexico.

VP WANG: No it wouldn’t! It’s Guam!

SEC GEITHNER: How about the Aleutians?

VP WANG: No!

SEC GEITHNER: Well, just keep it in mind. Anyway, as I said today at the University, we’re committed to keeping a strong dollar, and –

VP WANG: (snaps at Geithner in Chinese)

SEC GEITHNER: (pauses; looks at translator)

TRANSLATOR: Uh … the vice-premier said he is certainly glad to hear of your commitment to your wise and well-considered strong dollar policy.

SEC GEITHNER: That’s not what he said.

TRANSLATOR: Uh …

SEC GEITHNER: Come on, what did he say?

VP WANG: “Bitch, please.” That’s what I said! You owe us $768 billion! And we all know you’re going to stealthily inflate its value away to nothing! Then where are we going to be? We’re going to have $768 billion worth of fancy covered toilet paper!

ASST. VP YU: And what the hell are we doing meeting here, anyway? I mean, here we have 768 billion of your dollars, and we can’t even go down to McDonald’s and get a hamburger. We should be meeting some place cool, like San Diego!

(General agreement among Chinese delegation).

ASST. VP YU: I mean, that would rule. Or Las Vegas. Can you imagine how cool it would be if we got to go to Las Vegas with like $100 billion? That would kick ass.

CHINESE DELEGATE: We always meet here! I wanted to visit Graceland!

SEC GEITHNER: You invited us!

VP WANG: Yes, because it was polite! But you were supposed to say you were busy and then invite us there for a rain check! Honestly, do you know nothing about how things work?

SEC GEITHNER: Oh, so now we’re supposed to read your minds. I see.

VP WANG: God, you’re worse than the French.

SEC GEITHNER: OK, so let’s talk for a bit. Let’s say we did go a bit crazy with the whole “creating money out of thin air” thing. So if we did that, wouldn’t that cause the yuan to eventually appreciate against the dollar?

VP WANG: Well, yeah, but not by much, because we’re not going to –

SEC GEITHNER: Work with me here. Now, I know that you know that I know that you’re manipulating your currency to keep it artificially cheap, and you do that by … oh, buying dollars. Isn’t that right? I mean, we’re cool with that, but doesn’t the stability of your economy depend on strong growth and job creation?

VP WANG: Well, we’re working on –

SEC GEITHNER: I mean, I forgot, how many of your citizens are living in impoverished rural areas? Oh, that’s right, 800 million or so?

VP WANG: That’s not relevant to our …

SEC GEITHNER: Aren’t most of those 800 million people really angry?

VP WANG: They’re not angry! They’re just ... well, slightly upset.

SEC GEITHNER: Well, guess how angry they would be if their friends and family members in the industrialized east all lost their jobs because Chinese goods would become super expensive to foreigners, and all the multinationals went elsewhere for their manufacturing needs? I’m not saying, I’m just saying.

VP WANG: Please. Where are the multinationals going to go? North Korea? Good luck with that. They’d get halfway through a production shift and everyone would have to go study the Wise and Glorious Revolutionary Principles of Great General Kim Jong-il, Steward of the Juche Idea.

SEC GEITHNER: They do that on their own time. There’s no overtime in North Korea!

VP WANG: Well, you’re still full of –

SEC GEITHNER: No, I’m not! You know full well what would happen if you stopped buying our Treasuries. Do you want 100 million angry people marching on the capital demanding work?

(Silence).

VP WANG: You know, we could use a few passenger jets.

SEC GEITHNER: How about Yellowstone?

In related news, the People’s Daily newspaper announced today that 43 students who attended Secretary Geithner’s lecture have been volunteered to pursue extended studies at Harmonious Agricultural Labor Camp No. 19 in Xinjiang province.

June 01, 2009

Today's "Alex" Cartoon Nails It

TODAY'S VERSION of "Alex" -- the long-running cartoon in The Telegraph which looks at financial markets -- pretty much nails the reasons behind the sudden rash of pessimism we're seeing about the markets' future.

An Editor's Pick in This Week's Carnival of Personal Finance

I ABOUT FELL off my chair this morning when I logged on to this week's Carnival of Personal Finance and found I was not only an editor's pick, but the first-listed entry in the entire carnival -- which gets more than 100 submissions each week from a variety of talented writers. That's pretty damn cool, and I offer my sincere thanks to this week's host, "Funny About Money," which gave me a nice plug for my post below -- and which the host declared "too, too good!"

May 29, 2009

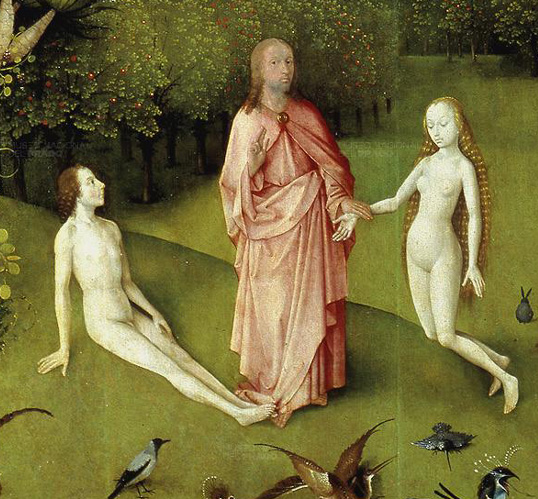

The Garden of Financial Delights

IN THE BEGINNING God created risk and return. And the risks were myriad and treacherous, and darkness was upon the face of the deep. And the spirit of God moved upon the face of the waters and said, “Let there be profit.” And God saw the profit, and saw that it was good; and He divided its sources into debt and equity. And the debt He called bonds, and the equity He called stocks. And the bonds and the stocks were the first instruments.

And the LORD God took the man, and did shew him the market, and put him into the market to dress and to keep it. And the LORD God commanded the man, saying, “Of every sector of the market thou mayest reap rewards. But of the Sector of Alternative Investments, thou shalt not reap from it; for in the day thou reapest thereof thou shalt surely die.”

Now the salesman was more subtle than any man which the LORD God had made. And he said to the man, “Behold, art thou earning but a pittance on thy savings accounts, and on thy muni bonds, and did not Business Week proclaim the death of equities?” And the man said, “Don’t remind me.” And the salesman said, “Thou should invest in the Sector of Alternative Investments, for thou canst reap great rewards many times that of the market, if only thou let me use the Fount of Leverage and draw from the River Forex and conjure Forces from the Pit of Shortselling.” And the man said, “Just what type of great rewards are we talking about?”

Verily the salesman looked at him and said, “Behold, I shall give thou the world and everything in it, and all for a mere two percent each year and twenty percent of the gains.” And the man said, “We’re good.” And lo, the salesman did go and produce great gains, and drew succor from all parts of the earth, and other men clamored to invest. And the salesman did create something from nothing, and all were in awe of his power; and the salesman went on to create funds of funds, which did the same thing but took even larger fees. Then men said to themselves, “Behold, the Sector of Alternative Investments is vast and powerful; and who can stand against it?” For those who controlled it had rode the bull and tamed the bear, and were portrayed in Fortune.

And the LORD God called to the man and said, “What is this thou hadst done? Didn’t I tell thou to stick with slow and steady growth?” And the man said, “Ooooooh, slow and steady growth. My fund’s alpha is through the roof and I’m partying at a mansion tonight with all these models from Eastern Europe.” And the LORD God looked at the man, and said, “Thou shalt reap what thou have sowed.” And the man looked at the LORD and wondered, but quickly dismissed the LORD’s chastisement, for the man didst score frequently with girls he met at nightclubs and partook of the Pool of Bollinger and Moet & Hennessy.

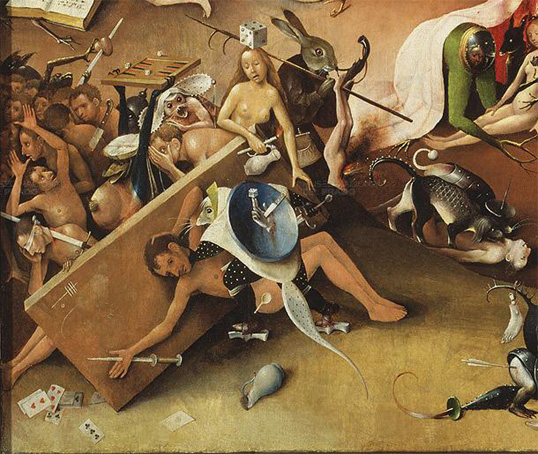

But the man had forgotten about the serpent, who stalked the fields and offered his money to those who dwelt in rental units and smallholdings, saying, “Come, thou can afford a dwelling of thine own, or I can refinance thou mortgage and bring thou vast wealth.” And the people said, “Really?” And the serpent said, “Yea, verily, for the housing market always goes up.” And the multitudes did rejoice and bought flat-screen televisions and went on cruises and traded up to sport-utility vehicles.

But the multitudes were overcome with fear when their mortgages reset, and hid in their dwellings from their creditors. And they cursed the serpent, and there was much wailing and gnashing of teeth, and they feared being cast into the outer darkness. And the storekeepers and the merchants and the industrialists all wondered at this, and said, “Oh, shit.” And the LORD opened the gate to the Pit, and a black smoke arose from it, and the man heard a voice crying, “One month LIBOR for 4.5 percent, and three month LIBOR for five percent, but oil will crash from $145 to $50 a barrel.”

Then it came to pass there was a great earthquake in the markets, and the sun turned black like sackcloth, and the moon was as if it was made of blood. The stars in the sky fell to earth, and the sky receded like a scroll, and every stock and mutual fund and hedge fund was removed from its place. Then the kings of the earth, the princes, the generals, the rich, the mighty, and every free man hid in caves and among the rocks of the mountains, and called to the Fed, “Hide us from the wrath of the Great Deleveraging, for the great day of its wrath has come, and who can stand against it?”

And the Fed did act, but it was too late for the man, who wept and beseeched the LORD for succor, saying, “LORD, forgive me, for I have sinned and didn’t really expect the whole risk thing while I was enjoying my returns.” And the LORD hid His face from the man, and cursed him, and sent him forth covered in sore boils and leprosy; and the man was ruined, and cursed his fate and the markets and the day of his birth. Thus the man left the presence of the LORD, and dwelt in the land of Nod, which is just outside Toledo, and became a vagabond, amidst the ravaged multitudes.

----------

(Details from Hieronymous Bosch, "The Garden of Earthly Delights," c. 1504)

May 21, 2009

Rubbing Salt in the Wound

AS A WRITER, I know perfectly well the importance of a good lead. Properly executed, it can draw in readers to a story they would otherwise ignore. It can soften the heart, it can inspire the imagination, and in some cases, it can cause one's blood to boil and prompt a frantic search for one's nitroglycerin.

With his incendiary introduction to an otherwise sedate essay on the economics of journalism, Robert Picard could not have succeeded any better in drawing that last reaction out of his targeted readership.

You see, in the pages of the Christian Science Monitor, Prof Picard has argued that journalists deserve low pay for their work, arguing it has little economic value. He could not have garnered more attention if he had walked into a newsroom, pulled a fire alarm, stripped off his clothing and preached his gospel whilst standing on the police reporter's desk. Prof Picard writes:

Journalists like to think of their work in moral or even sacred terms. With each new layoff or paper closing, they tell themselves that no business model could adequately compensate the holy work of enriching democratic society, speaking truth to power, and comforting the afflicted.Actually, journalists deserve low pay.

Wages are compensation for value creation. And journalists simply aren't creating much value these days.

Until they come to grips with that issue, no amount of blogging, twittering, or micropayments is going to solve their failing business models.

Gee. Thanks for the tip, Mr Helpful.

Of course, if one was cynical -- and I am certainly not -- one might point out that Prof Picard is a professor of media economics at something called Jonkoping University in Sweden. As such, he is rather ballsy to suggest that journalists are deserving of low pay, as most academics produce little to nothing in the way of economic value. 90 pc of their research is published in obscure journals and forgotten; 90 pc of their insights are so specialized as to be meaningless to the general public or even educated laymen; 90 pc of their work does nothing to advance the human condition. True, there is value in their teaching; but even then, most of the work is fobbed off on starving graduate students, whilst the tenured professor spends his days ruminating on the modern-day relevance of Marx and Fanon.

Prof Picard tries to weasel out of this; he argues journalists do not have specialized knowledge, such as "professors" and "electricians" do. But comparing academics to electricians is an insult to electricians. Besides, there is no denying whose labor is more valuable when one's electricity fails and you have a refrigerator full of perishables.

Also, I would take issue with Prof Picard's characterization of how journalists view their work. My view may be different than most in the field, as I'm a now-underemployed business journalist, but I've never considered my work a holy calling. Certainly I don't value it enough to take a vow of poverty along with the job. When I covered business, my job was simple: present facts and useful information to my readers so they could then make informed decisions about their finances or business operations. For that matter, that's how I approached every other topic about which I wrote.

Still, I don't mean to slight Prof Picard's argument too much. When it comes to the larger points, he is right: media companies and the journalists who work for them must provide economic value to their readers. Otherwise, the readers won't buy what they're selling. As Prof Picard writes:

Well-paying employment requires that workers possess unique skills, abilities, and knowledge. It also requires that the labor must be non-commoditized. Unfortunately, journalistic labor has become commoditized. Most journalists share the same skills sets and the same approaches to stories, seek out the same sources, ask similar questions, and produce relatively similar stories. This interchangeability is one reason why salaries for average journalists are relatively low and why columnists, cartoonists, and journalists with special expertise (such as finance reporters) get higher wages.Across the news industry, processes and procedures for news gathering are guided by standardized news values, producing standardized stories in standardized formats that are presented in standardized styles. The result is extraordinary sameness and minimal differentiation ...

... If value is to be created, journalists cannot continue to report merely in the traditional ways or merely re-report the news that has appeared elsewhere. They must add something novel that creates value. They will have to start providing information and knowledge that is not readily available elsewhere, in forms that are not available elsewhere, or in forms that are more useable by and relevant to their audiences.One cannot expect newspaper readers to pay for page after page of stories from news agencies that were available online yesterday and are in a thousand other papers today. Providing a food section that pales by comparison to the content of food magazines or television cooking shows is not likely to create much value for readers. Neither are scores of disjointed, undigested short news stories about events in far off places.

In other words, media firms must make use of their comparative advantages if they want to succeed. A newspaper in Poughkeepsie, for instance, ought focus on Poughkeepsie -- because that's what's important to its readers: not, as Prof Picard points out, day-old wire copy repeating what they've already seen on-line or on television.

May 20, 2009

Your Money and You

Oh No!

It’s Time for Yet Another Edition of …

YOUR SEARCH ENGINE QUERIES ANSWERED!

An occasional Rant feature

IT WOULD APPEAR that my most recent installment of Your Search Engine Queries Answered! was, to use the technical term, a hit. Readership is up, it got a nice mention on something called Twitter, and people seemed generally pleased with it.

Thus, I’m going back to the well again for a special second round of Your Search Engine Queries Answered! Today, we’re going to look mostly at matters dealing with finance and economics. Why, you ask? Well, it was the most popular topic the last time. Reason enough for me. Besides, in these tough economic times, more people than ever hope to understand how our economy works. I’m happy to help. So, without further ado, let’s go to this edition of … Your Search Engine Queries Answered!

QUERY: assume that smith deposits $600 in currency into her checking account in the xyz bank. later that same day jones negotiates a loan for $1 200 at the same bank. in what direction and by what amount has the supply of money changed?

ANSWER: The supply of money will increase by $900. Here’s why.

Smith has put her money into a checking account, which means the bank will treat it as payable on demand and won’t loan any of it out. Thus the net increase there is zero. As for Jones, although he might negotiate a $1,200 loan at his branch, he’ll find out later the loan officer will get overruled by his boss, who is under orders not to actually loan money. This is because his boss’s boss is under orders from his boss not to loan money because the bank is trying to repay its TARP money, which the Treasury tricked it into taking.

However, when the bank tries to repay its TARP money, the Treasury tells it not only to pound sand, but that a senator from the bank’s state is holding a hearing on why it isn’t loaning out any money. So then the bank goes back and argues internally, and eventually decides that it can loan out Jones $900. Jones then takes his $900 and hides it under his mattress, thus technically adding it to the local money supply but really just contributing to the Paradox of Thrift that has been destroying our economy. Q.E.D.

QUERY: what is jpmorgan chase & co.’s p/e ratio hypothetically if the company issues equity in order to raise $10 million of capital?

ANSWER: The same as it was before, for all intents and purposes. What is $10 million to the House of Morgan?

QUERY: nonincentive stock option sell to cover

ANSWER: As a general rule, you should think about selling enough of your options to pay the appropriate tax due on them. Otherwise, you’ll end up like all those techies when the dot-com bubble burst, who owed oodles of tax when their options for nobusinessplan.com vested at $89 each and then went to zero in little under a year. No one’s going to mind if you do this.

QUERY: what are the markets going to do next week

ANSWER: Ah, the timeless question: how will the markets do next week? I have no idea. So I turned to the I Ching, the ancient Chinese book of divination, and posed it your question. The I Ching said:

The present is embodied in Hexagram 5 - Hsu (Waiting): With sincerity, there will be brilliant success. With firmness there will be good fortune, and it will be advantageous to cross the great stream. The third line, undivided, shows its subject in the mud close by the stream. He thereby invites the approach of injury. The situation is evolving slowly, and Yin (the passive feminine force) is gaining ground.The future is embodied in Hexagram 60 - Chieh (Limitation): There will be progress and attainment, but if the regulations prescribed be severe and difficult, they cannot be permanent.

The I Ching thus tells us that he who holds the line, and does not sell his shares in a panic, will garner great wealth and fortune in the long term. The mud by the stream represents institutional investors and hedge funds, who are targeting certain sectors -- *cough* commercial real estate *cough* – and may decide to go super-short on them, thus causing much distress and anguish to those who can’t bear to see their real-estate fund drop nine percent in a day. An increase in Yin represents selling pressure and caution among small retail investors, who would prefer not to lose any more of their money.

As for the future, this shows there will be upward momentum among financials, unless the Government steps in and crushes them under its foot. The I Ching has spoken. Behold its wisdom.

QUERY: on the pernicious speculation action and corresponding supervising countermeasures in the stocks market of china

ANSWER: As a market, China scares the hell out of me. For one thing, like any emerging market, it is prone to speculative bubbles, and if I remember right, it had a good one going until the Reds took the air out of it. This leads to the second reason why I’m scared of it – China’s Government makes Darth Vader look slow to act when it comes to changing the terms of a deal midway through. So you can keep Shanghai and Shenzhen, for all I’m concerned.

QUERY: how much money did it take to make xenia back to normal after 1974 tornado

ANSWER: Since when was Xenia normal? I mean, come on.

QUERY: hey bloated rates

ANSWER: How can this commercial STILL not be on YouTube? It was a classic. This was the one for Brown & Co. where the lady comes in and wants to trade on margin, and the front-office doofus thinks she wants to trade butter. (“No, MARGIN!” “Oh, right.”)

Oh, speaking of commercials you could see on CNBC all the time, here’s one for … well, I was hoping this would be a surprise, but NOOOOO -- YouTube's stupid preview screen ruins it. But hey! It's Smilin' Bob!

I loved these commercials, if only because they're so downright ... blatant. (Readers at work might want to turn off the sound or wear headphones, if only so your colleagues don't get any funny ideas). As for why these commercials aired constantly on the all-stocks channel ... well, I'll leave that for readers to discuss!

QUERY: operational research decision tree for an orange owner in florida faces a dilemma. the weather forecast is for cold weather and there is a 50% chance that the temperature tonight will be cold enough to freeze and destroy his entire crop, which is worth some $50 000. he can take two possible actions to try to alleviate his loss if the temperature drops. first he could set burners in the orchard; this would cost $5000 but he could still expect to incur damage of approximately $15 000 to $20 000. second he could set up sprinklers to spray the trees. if the temperature drops the water would freeze on the fruit and provide some insulation. this method is cheaper $2000 but less effective. with the sprinklers he could expect to incur as much as $25 000 to $30 000 of the loss with no protective action. compare the grower s expected values for the three alternatives he has. which alternative would you suggest the grower take? why?

ANSWER: The orange grower should take none of these steps, and instead make a claim against his insurance in the event of a catastrophic frost. Barring that, he should apply for disaster aid from the Government, allowing him to get his $50,000 back at a nominal rate of interest, which would cost him just a couple of thousand dollars per year.

QUERY: never donate to alma mater

ANSWER: Good decision! One should only donate to one’s alma mater if one can deduct it from one’s taxes and wants really good football tickets.

QUERY: what does audibilize mean?

ANSWER: “Audibilize” is an Americanism that means the quarterback is improvising and has changed the previously-agreed upon play, known as “calling an audible.” For more on this, look under “trickeration” in your General Dictionary of American English.

QUERY: can a film director rewrite a script?

ANSWER: Not only can he rewrite the script, he can screw you out of your writer’s credit if he’s clever enough. So unless you want a “based on an idea by” credit, call your lawyer.

QUERY: how much is a legitimate markup

ANSWER: As much as you can get away with, just up to the point where people start thinking you’re a real jerk.

QUERY: i did everything right then everything went wrong

ANSWER: Ah, yes. I know the feeling! The important thing to remember is that you’ll rebound from this.

QUERY: how to speculate currency

ANSWER: Currency speculation isn’t my thing. But if you’re interested about this and other matters related to market trading, you might want to visit the good people at TTS Trading Ltd. in Vancouver, B.C. TTS Trading Ltd., according to its Web site, provides "insight, intelligence, and education for the self-directed active trader" – and they gave me a shout-out on Twitter for my last Your Search Engine Queries Answered! This sent bunches of readers my way. Thanks, guys!

QUERY: you have just noticed in the financial pages of the local newspaper that you can buy a $1 000 par value bond for $800. if the coupon rate is 10 percent

ANSWER: This is a trick question, because local newspapers don’t print bond listings any longer.

QUERY: i am consuming 50000 gallons/month of water. is this good

ANSWER: No, it’s not good, you stupid prat! What are you wasting that on, a replica of the fountains in front of the Bellagio? Also, you’re going to have the inspectors from the water utility fining you for your stupid manicured lawn.

QUERY: report in how to spend ur money economicly

ANSWER: Spend less than you earn. Next!

QUERY: guy billed $62 000 for downloading wall-e

ANSWER: I’m sure he deserved it.

QUERY: canadian football league run by idiots

ANSWER: Well, I can’t disagree with you there, if only because – once again! – I can’t get any telecasts of the CFL’s games this year. Jesus Christ. The season starts in July. That’s two months of real football I could be watching but can’t, and so I’ll have to listen to the games on Internet radio again.

QUERY: indoor football games fun to watch?

ANSWER: YES. Particularly in person. Get a seat a few rows up – trust me on this, because you don’t want a linebacker flying into your seat – but not too far up, and you’ll find it exciting and thrilling.

QUERY: american idol broadcast in san miguel allende mexico

ANSWER: You’re in San Miguel and you want to watch American Idol? Are you well? I mean, come on. You’re in San Miguel. The only television shows you’re allowed to watch are sports broadcasts and CNBC.

QUERY: summary of rich dad poor dad gold miner advice

ANSWER: Who the hell ever heard of asking a gold miner for financial advice? I mean, really. Here you have Prospector Jed out in Death Valley panning for gold or something, and twenty years later he’s … still out panning for gold. I mean, let’s get realistic here.

QUERY: towels are kinda scratchy meaning

ANSWER: Congratulations, Verizon – your advertisement has now become a topic for philosophers to debate.

QUERY: is a television a durable good?

ANSWER: You mean the box itself or what’s on it?

QUERY: goodwill inadvertant unwind

ANSWER: How do you inadvertently unwind goodwill? It’s goodwill. It sits on the balance sheet and does nothing. Well, OK, it reminds a company it overpaid when it ate a smaller company, but other than that, it doesn’t have any intrinsic value. And what if it’s negative? Then what? Do you have “badwill?” Actually, that’d be kind of cool on a balance sheet.

QUERY: next week market forecast

ANSWER: Oh, not this again. All right, here we go. A moment, please.

All right, I’m ready. The I Ching said:

The present is embodied in Hexagram 14 - Ta Yu (Possession in Great Measure): There will be great progress and success. The topmost line, undivided, show its subject with help accorded to him from Heaven. There will be good fortune, advantage in every respect. The situation is evolving slowly, and Yin (the passive feminine force) is gaining ground.The future is embodied in Hexagram 34 - Ta Chuang (The Power of the Great): It will be advantageous to be firm and correct.

Well. I suppose this means … BUY! BUY! BUY! Clearly the I Ching means that buy-and-hold investors will be rewarded for their fortitude, because Hexagram 14 indicates institutional investors and hedge funds will all start going long. Unless, of course, the I Ching means that we’re all doing pretty well now, but that the hedge funds will all go short and we’ll hemorrhage red ink out of our pores until the market eventually turns around.

That’s it for this edition of Your Search Engine Queries Answered! Tune in next time, when we examine the foibles of Terrell Owens, why it’s a bad idea to do electrical work at home, and our standard boilerplate policy on financial matters, which is this:

DISCLAIMER: This entry is not intended to act as financial advice or serve as a substitute for financial advice from a qualified certified financial planner or other knowledgeable professional. Investing can and does involve risk and carries with it a chance of losing all your money, as we’ve found out over the past several months. Buyer beware. And if it seems too good to be true, it probably is.

May 07, 2009

Winner Winner Chicken Dinner (or, KFC Rolls Big Red)

ATTENTION MARKETING FOLKS -- when you promise people free food, they're going to come out of the rafters to come get it. When you promise Americans free food, they're not only going to come out of the rafters, they're going to invite all their friends, have a tailgate party and celebrate at the good fortune Providence has bestowed upon them. Add in a recession, and well, it's going to cause a bit of a ruckus.

Along those lines, when you promise Americans free food, you had best have a LOT of it on hand. Otherwise, you're going to have a lot of unhappy Americans. And when Americans get unhappy ... well, it's not a pretty scene.

Consider what the poor people at Kentucky Fried Chicken are going through. They thought they had a marketing coup by getting Oprah Winfrey to advertise a giveaway in which people could receive two (2) free pieces of a "grilled" variant of their chicken. Now, why exactly anyone would buy "grilled" chicken at a fried-chicken outlet is beyond me, but there you go. And besides, it's free chicken.

Unfortunately, KFC apparently didn't adequately prepare for the onslaught of customers they would receive as a result of their promotion. Across the nation, people reported they couldn't redeem the Internet-based coupons they were told to get from the Internet. In New York, angry customers reportedly launched a sit-in upon not receiving their free chicken. In Annapolis, the giveaway was apparently being operated by managerial fiat, with predictably poor results. And it would appear, based on media coverage of this story -- 'cause it's one now -- that KFC's logo needs a "FAIL" stamp put on it.

Not only that, but El Pollo Loco came in and told KFC -- in so many words -- to step aside and let the professionals handle it. Oh, hell yeah.

Now, as a former California resident, I am quite familiar with El Pollo Loco, which is where people in the Golden State go if they want not-fried chicken. I can also say that, as a former California resident, I would go to El Pollo Loco over KFC any day of the week. Also, New Hampshire needs an El Pollo Loco, just like it needs an In-N-Out Burger, a Jack in the Box, and a Del Taco. Maybe El Pollo Loco will save me from what by all means can be considered a fast-food desert up here.

But I digress. Anyway, El Pollo Loco noticed that KFC's free chicken giveaway wasn't good on Mother's Day. I don't know why it's not, even though I personally would sooner cut off my own head rather than take a girl to KFC on Mother's Day. I have no desire to discover the secret recipe for sleeping on the sofa for three weeks. But anyway, El Pollo Loco came out and said, "Fine. If KFC has something against mothers, we'll honor the damn coupons on Mother's Day, plus throw in two side dishes and tortillas." Oh, snap.

Also -- as CNBC reports -- El Pollo Loco caught stupid people from KFC calling into their comment line and talking up the Colonel's product while denigrating the citrusy goodness of El Pollo Loco. Then El Pollo Loco went and made an ad about it, using the taped conversations and Caller ID information. ("Highway 5? In California, it's The 5.") Oh, snap.

Besides, as at least one commenter I saw pointed out, KFC serves Pepsi products. Ew. Coke is it, people --

-- or, if you're like me, Coke Zero, 'cause it has no sugar in it. Yeah.

May 05, 2009

Well, I Could Have It Worse

BY WHICH I MEAN, I don't live in Michigan, because the place is apparently turning into Mad Max Beyond Thunderdome.

Back home, according to no less a source than The Detroit News, my fellow Michiganders are engaged in a rather ghoulish kind of commerce for cash. They're selling their hair. They're selling their blood plasma. They're subjecting themselves to medical experiments. Women are even selling their eggs. At this rate, it shouldn't be much longer before Michiganders are selling their kidneys; after all, God has mercifully provided all of us with two of them, when we really only need one.

Of course, one could argue this type of commerce is not really ghoulish, since it involves willing participants on both sides and the articles being handled do not generally make up what economists call a "repugnant market." It's not, after all, as if the good people of Michigan are robbing graves to pay for their kids' college tuition. Still, even for a devotee of free markets like myself, it's kinda offputting.

Why, you ask? Well, I feel bad that anyone has to actually do those types of things for money. Also, I think these folks are getting a raw deal.

I have long thought the American system of "donating" blood and organs is a rather bad deal -- not so much for the recipients, but for the donors. A pint of blood goes for $150 or $200, so why shouldn't I, as a donor, get $30 or $40 for my rare type A-negative? After all, I'm the one doing the hard work.

Along those lines, I'm not exactly thrilled about the idea of being an organ donor, even though I am one. I've had second thoughts about this, but it'd be too much of a hassle to go down to the Department of Motor Vehicles and change it, so there you go.

Now, as you can imagine, I have no plans to die anytime soon. In fact, my own projections indicate I will live to 110 years of age, as I figure my strategic spite duct (a small organ next to the liver) has enough bile, ichor and sheer disgust stored in it to last me until 105 or 106. And even after that's exhausted, my desire to watch sports should prove a strong incentive not to kick the bucket.

But if, God forbid, I should die in an accident or something, why should my estate get nothing if I were to donate my skin, my bones, and my vital organs? I mean, some estimates place the worth of a human cadaver at no less than $200,000.

Now, I know I can't take it with me, but that's not the point. The point is that if I "donate" my dead body for medical uses, other people will profit off it while my estate gets nothing. What's up with that? I mean, it's almost as bad a deal as going to a strip club. And if there's one thing that annoys me in life, it's being on the wrong end of a bad deal. Just because I'd be dead does not mean I suddenly wouldn't have an interest in monetizing, well, me, particularly if it paid for a relative's college tuition. Or a really nice obelisk for my grave site. Or even a mausoleum. Yeah. With nice stained-glass windows, and a phone line in case I suddenly materialize and want pizza.

And if I'm not properly compensated for my monetization when I die, I'm warning you now -- I am going to come back and haunt the hell out of everyone. I'm serious.

MORGUE WORKER: That's odd.

SECOND MORGUE WORKER: What?

MORGUE WORKER: Got cold here all of a sudden.

SECOND MORGUE WORKER: It's just your imagination.

ME: Why you wretched -- ah, God, it's not working! Stupid incorporeal body! All I want to do is strangle him for a minute with my cold spectral hands!

DEATH: Ah, yes. There's a bit of a latent period before you can do that. No one told you?

ME: No, no one told me! And look at these invoices! I mean, I should get thirty thousand at least.

DEATH: Well, you've got a month to figure it out. After that, I get docked on my commission for delivering you late to Purgatory.

ME: Oh, well -- wait, what? You work on commission?

Of course, I don't mean to criticize anyone who is a willing blood or organ donor, and does so out of the goodness of one's heart. That selflessness is noble and the sacrifice is certainly valued. But given the waiting lists for organs, it seems pretty clear that donations aren't enough to get the job done. Also, it seems clear to me that our culture of donation serves up a pretty raw deal for people who are willing to literally give of themselves.

This goes particularly when it comes to women donating eggs. Obviously, they're doing a great service for the recipients, and offering a gift that in many ways is priceless. But as the News reports, the compensation they are given -- capped at $5,000 -- seems far too low to adequately address the very real risks they face. It's no joke to donate anything from one's body, and I think the least we could do to be fair about it would be to offer fair market values for the things donated.

April 08, 2009

Somali Pirates No Match for US Mariners

OK, HERE'S AN IMPORTANT SAFETY TIP for anyone considering a career in the growing field of maritime piracy: don't hijack an American-flagged vessel. That's not just because it will suddenly cause the world's sole superpower to take notice of your predations upon lawful commerce, but because the crew will fight back and ruin your plans well before Washington discovers something's up.

Apparently, the crew of the MV Maersk Alabama not only fought off the four armed Somali pirates that took over the ship, but managed to capture one and threw the remainder overboard. Sweet. That'll teach the Somali pirates to attack an American vessel. We've got your ransom right here, pal!

April 07, 2009

Maybe the Prosecutors Should Look Into Short Sellers

REUTERS: Two dozen charged in alleged gang-led mortgage fraud.

April 05, 2009

The End of the Affair

Those blues I lay low,

I'll make 'em stay low,

They'll never trail over my head;

I'll be a devil 'til I'm an angel,

but until then -- hallelujah!

-- Frank Sinatra

Like the sailor said, quote, ain't that a hole in the boat.

-- Dean Martin

ALL GOOD THINGS come to an end. In my case, the particular good thing that came to an end was my great job working as a reporter. It was interesting and engaging work, tough at times but also a lot of fun, and it was made even better by the great people with whom I worked. Plus, the pay and benefits I received were fantastic for the field, which made the work even better.

It wasn't entirely a surprise that I lost my job, of course. Since journalists love writing about themselves, the papers have been filled with stories about the troubles facing the media industry. So it's not as if I'm the only reporter to find himself studying up on rules and regulations about his unemployment benefit. Rather, I'm simply U.S. Media Sector Casualty No. 36,012 of the Global Economic Downturn. Business is business, and when you're at the bottom of the seniority list, these things can happen. So I certainly don't have any hard feelings about it, particularly since my employer kept me on as long as it could in my job.

That's not to say I don't feel any sense of loss, though. For a while yesterday -- yesterday being "the day after" -- I was feeling a bit lost, and a bit down about the whole thing. Fortunately, thanks to the Power of Technology, I can kind of show you how I felt for a few hours! Let's roll the clip:

Now, I know what you're thinking. "Kepple! You don't look anything like Joey Bishop!" Well, this is true. I just love that scene; the final contemplative walk in defeat. But I've got that out of my system and now I can move forward.

This is, of course, what one must do in a situation like this.

The way I see it, one has two options. You can feel sorry for yourself, and let the gloom drag you down into a deep funk, even though that leads to a variety of unfortunate things -- like growing a recession beard*, and watching daytime television, and lying on the sofa, and not showering regularly. Alternatively, you can pick yourself up, dust yourself off, spend a few days relaxing and then develop a plan to get back in the game. Personally, I think the second option is the better one.

This goes especially when you think about the great run I had over the last eight years. I mean, my God. When I think about what I was able to do, what I was able to see, who I was able to meet and interview -- I couldn't have asked for anything better. I hit more than one home run in my day and I'm proud of the work I did. Not only that, I went into it pretty darn green -- but when I came out, I came out with a whole set of new skills and experiences that taught me a hell of a lot.